Digital payments are no longer just a transaction layer — they are a growth engine. In 2026, businesses expect payment processors to do far more than process cards. They must reduce friction, prevent fraud, support global expansion, and integrate seamlessly with business systems.

With dozens of payment processors available, choosing the right one can directly impact conversion rates, customer trust, and operational efficiency. This guide breaks down the top 10 payment processors in 2026, explains what each does best, and helps you decide which solution aligns with your business goals.

Why Payment Processors Matter More Than Ever

Customer expectations around payments have changed dramatically. Users want instant checkouts, local payment options, and strong security — all without visible friction. On the business side, companies need better reporting, faster settlements, and compliance across multiple regions.

Modern payment processors now act as:

- Revenue optimization tools

- Fraud prevention systems

- Infrastructure for global commerce

- Platforms for embedded financial services

Choosing the wrong processor can increase cart abandonment, chargebacks, and operational costs. Choosing the right one can unlock scale.

Top 10 Payment Processors in 2026

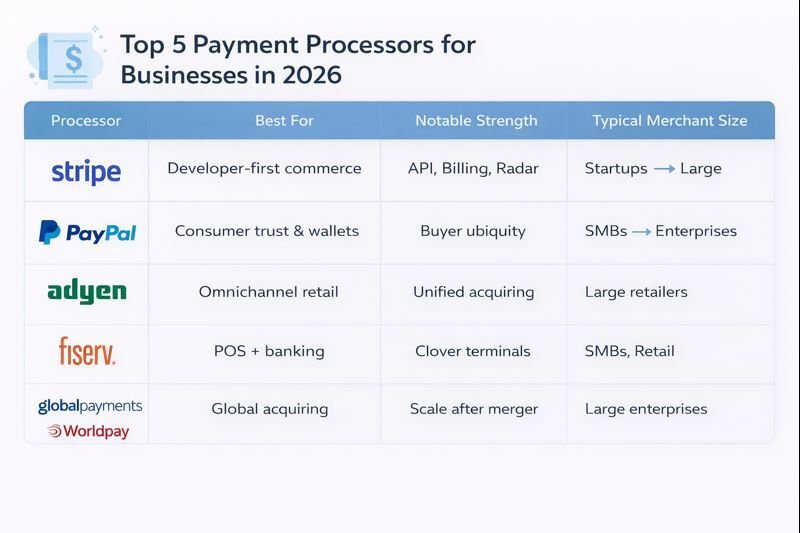

1. Stripe

Stripe continues to lead the market with its developer-first approach and highly flexible payment infrastructure. Its APIs allow businesses to design customized payment flows, manage subscriptions, support marketplaces, and accept payments in multiple currencies.

Stripe also provides advanced fraud detection, recurring billing, tax automation, and payout management — making it more than just a payment processor.

Best for:

Technology companies, SaaS platforms, startups, and global marketplaces

Key strengths:

- Powerful APIs

- Global currency and payment method support

- Scalable for fast-growing businesses

2. PayPal

PayPal remains one of the most trusted payment brands globally. Its massive consumer user base makes it a strong conversion driver, especially for e-commerce businesses. Many customers prefer PayPal due to its perceived security and ease of use.

Beyond checkout, PayPal supports digital wallets, pay-later options, and peer-to-peer payments through its ecosystem.

Best for:

E-commerce stores, small to mid-sized businesses

Key strengths:

- High consumer trust

- Quick setup

- Wallet-based checkout options

3. Adyen

Adyen is designed for large enterprises that operate across channels and regions. Its single-platform model supports online, in-store, and mobile payments while providing centralized reporting and analytics.

Adyen’s strength lies in data optimization — helping businesses improve authorization rates and reduce payment failures at scale.

Best for:

Large retailers and multinational enterprises

Key strengths:

- Unified omnichannel payments

- Enterprise-grade analytics

- High transaction reliability

4. Global Payments / Worldpay

Following industry consolidation, this combined entity has become a major force in merchant acquiring and enterprise payment services. The platform supports businesses operating across multiple markets and industries.

Its broad infrastructure makes it suitable for companies that need global reach with local acquiring support.

Best for:

Large enterprises and global merchants

Key strengths:

- Wide geographic coverage

- Strong acquiring network

- Enterprise scalability

Read More: Top 10 Payment Gateway Software Development Companies in 2026

5. Fiserv

Fiserv offers a unique blend of payment processing, point-of-sale systems, and financial technology services. Its Clover POS platform is widely adopted by physical retailers and restaurants.

By combining payments with hardware and banking integrations, Fiserv simplifies operations for businesses with in-store presence.

Best for:

Retailers, restaurants, and SMBs

Key strengths:

- Integrated POS and payments

- Strong banking relationships

- Omnichannel support

6. Block (Square)

Block, formerly Square, focuses on small businesses and sellers who need simple, flexible tools. Its ecosystem includes card readers, POS software, payroll, invoicing, and business analytics.

Block has expanded beyond payments to support end-to-end commerce for small merchants.

Best for:

Small businesses, cafes, mobile sellers

Key strengths:

- Easy onboarding

- Affordable hardware

- All-in-one business tools

7. Checkout.com

Checkout.com has emerged as a strong global challenger, particularly for high-growth e-commerce businesses. Its cloud-native architecture allows fast integrations and performance optimization across regions.

The platform emphasizes transparency, payment performance, and merchant control.

Best for:

International e-commerce and digital-first brands

Key strengths:

- High authorization rates

- Global coverage

- Developer-friendly APIs

8. Payoneer

Payoneer specializes in cross-border B2B payments and international payouts. It is widely used by marketplaces, freelancers, and companies paying suppliers across multiple countries.

Unlike traditional processors, Payoneer focuses more on disbursements than consumer checkout.

Best for:

Marketplaces, global contractors, B2B payments

Key strengths:

- Multi-currency payouts

- International compliance support

- Cost-effective cross-border payments

9. FIS

FIS is a major provider of payment processing and banking infrastructure. It supports issuing, acquiring, and core banking services, making it a strong choice for financial institutions and enterprises building embedded finance products.

Its strength lies in scale, compliance, and institutional partnerships.

Best for:

Banks, fintech platforms, large enterprises

Key strengths:

- Deep banking integrations

- Issuing and acquiring services

- Regulatory expertise

10. Worldline

Worldline is a dominant player in the European payments market, particularly in terminal-based and contactless payments. Its services are widely used by retailers and service providers across Europe.

Worldline continues to focus on payment terminals, acquiring, and regional payment schemes.

Best for:

European merchants and retailers

Key strengths:

- Strong European presence

- Terminal and acquiring expertise

- Local payment method support

How to Choose the Right Payment Processor

Choosing a payment processor should be a strategic decision. Consider the following factors:

1. Business Model

SaaS, e-commerce, marketplaces, and brick-and-mortar businesses all have different requirements.

2. Geographic Reach

If you serve international customers, ensure the processor supports local currencies and payment methods.

3. Integration Requirements

Developer-heavy platforms benefit from API-driven solutions, while small businesses may prefer plug-and-play systems.

4. Pricing Structure

Understand transaction fees, cross-border charges, chargeback fees, and payout timelines.

5. Fraud and Security

Advanced fraud prevention and compliance tools are essential for long-term scalability.

Final Thoughts

Payment processing is no longer a backend function — it is a competitive advantage. The best payment processors in 2026 are those that align with your growth strategy, customer expectations, and operational complexity.

Whether you’re launching a startup, scaling an enterprise, or expanding globally, selecting the right payment processor can improve revenue, reduce risk, and future-proof your business.

Read More: Top Payment Gateway Development Companies in New York